Breakdown point in pictures

The breakdown point of an estimator is the largest fraction of the data you can replace with arbitrary outliers before the estimate becomes useless. It’s a theoretical guarantee, but it has a very concrete operational meaning: sweep contamination from zero to something high, fit your method at each level, and watch where the estimate stops tracking the true value.

Theoretical breakdown points:

Method |

Breakdown |

Why |

|---|---|---|

OLS |

0% |

A single huge outlier can move the fit arbitrarily far. |

Huber-M |

0% in |

Bounded loss helps on small-amount Y-only contamination, but no protection against high-leverage points. |

Theil-Sen |

~29% |

Median-of-slopes; breaks once contamination reaches the median. |

MM (bisquare default) |

50% |

The S-init step’s design is half the data; you’d need to corrupt more than half before MM falls. |

We’ll measure these by sweeping the contamination fraction.

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from pylmrob import lmrob, Control

import statsmodels.api as sm

from statsmodels.robust.robust_linear_model import RLM

from sklearn.linear_model import TheilSenRegressor

rng = np.random.default_rng(0)

plt.rcParams.update({"figure.dpi": 110, "axes.grid": True, "grid.alpha": 0.3})

METHODS = ["OLS", "MM (pylmrob)", "Huber-M", "Theil-Sen"]

COLORS = {

"OLS": "#d62728",

"MM (pylmrob)": "#1f77b4",

"Huber-M": "#ff7f0e",

"Theil-Sen": "#2ca02c",

}

Setup

For each contamination fraction eps in {0.00, 0.05, 0.10, ..., 0.50}, generate a clean dataset of n=200 then replace

floor(eps * n) of the y values with large outliers

(y = 50 + N(0, 1)). Fit each method, record the slope. Repeat 25

times per eps and report the median + IQR.

def fit_slope(x, y, method):

X = sm.add_constant(x)

if method == "OLS":

return sm.OLS(y, X).fit().params[1]

if method == "MM (pylmrob)":

df = pd.DataFrame({"x": x, "y": y})

return lmrob("y ~ x", df, control=Control(), seed=42).coef_[1]

if method == "Huber-M":

return RLM(y, X, M=sm.robust.norms.HuberT()).fit().params[1]

if method == "Theil-Sen":

return TheilSenRegressor(random_state=0).fit(

x.reshape(-1, 1), y).coef_[0]

raise ValueError(method)

def contaminate_y(rng, x, true_intercept, true_slope, eps):

"""Generate (x, y) with fraction ``eps`` of y values replaced by outliers."""

n = len(x)

y = true_intercept + true_slope * x + 0.5 * rng.standard_normal(n)

n_bad = int(np.floor(eps * n))

if n_bad > 0:

idx = rng.choice(n, size=n_bad, replace=False)

y[idx] = 50.0 + rng.standard_normal(n_bad)

return y

def sweep(eps_grid, n_rep=25, n=200, true_intercept=2.0, true_slope=1.5):

"""Return slope estimates as a (len(eps_grid), n_rep, len(METHODS)) array."""

sim_rng = np.random.default_rng(42)

x = np.linspace(0, 10, n)

out = np.empty((len(eps_grid), n_rep, len(METHODS)))

for i, eps in enumerate(eps_grid):

for r in range(n_rep):

y = contaminate_y(sim_rng, x, true_intercept, true_slope, eps)

for j, m in enumerate(METHODS):

out[i, r, j] = fit_slope(x, y, m)

return out

eps_grid = np.linspace(0.0, 0.5, 11)

slopes = sweep(eps_grid)

slopes.shape # (11, 25, 4)

(11, 25, 4)

Result

median = np.median(slopes, axis=1) # (11, 4)

q25 = np.quantile(slopes, 0.25, axis=1) # (11, 4)

q75 = np.quantile(slopes, 0.75, axis=1) # (11, 4)

fig, ax = plt.subplots(figsize=(8, 5))

for j, m in enumerate(METHODS):

ax.plot(eps_grid, median[:, j], lw=2, color=COLORS[m], label=m)

ax.fill_between(eps_grid, q25[:, j], q75[:, j],

color=COLORS[m], alpha=0.18)

ax.axhline(1.5, color="gray", ls="--", lw=1, label="true slope")

ax.set_xlabel("contamination fraction ε")

ax.set_ylabel("estimated slope (median ± IQR across 25 reps)")

ax.set_title("Slope estimate vs contamination level")

ax.legend(fontsize=9, loc="lower left")

fig.tight_layout()

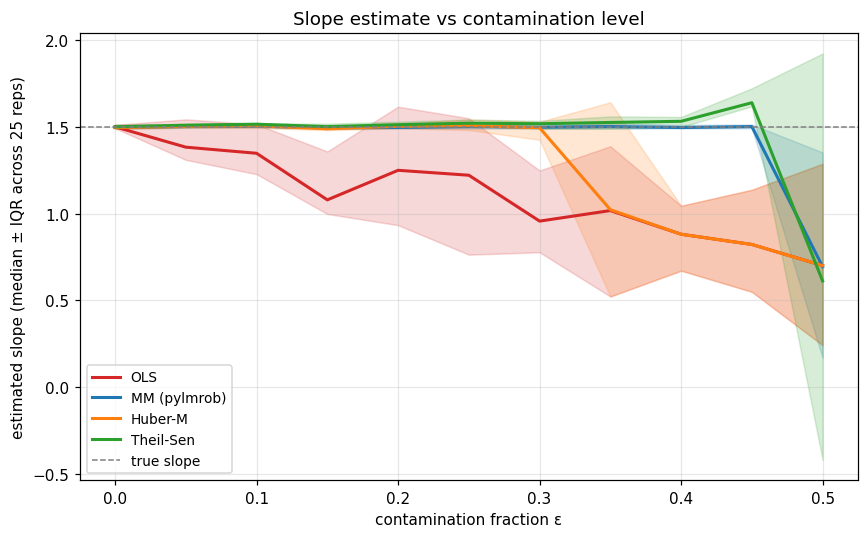

Reading the picture.

OLS drops the slope linearly. Even at ε=0.05 it’s already off. It has no notion of “outlier”.

Huber-M holds the slope close to 1.5 for a while — Huber’s bounded loss can absorb a few bad Y values — then drops as the contamination grows past ~25%. Its breakdown point is technically zero (a single bad point at high leverage can ruin it), but in this Y-only contamination scenario the operative bound is a fraction.

Theil-Sen holds until ε ≈ 0.29 (its theoretical breakdown), then collapses sharply.

MM stays close to the truth across the entire range. At ε very close to 0.5 it starts to wobble — the S-step’s half-the-data resampling has trouble finding clean half-subsamples — but it remains by far the best of the four.

The “cliff” at the breakdown point isn’t a soft boundary. Once the contamination passes the limit, the estimator’s design assumptions fail and the output is meaningless.

What ε=0.5 means in practice

A 50% breakdown point sounds like a lot of headroom. In real datasets it’s quite ordinary to have 1-5% contamination from data entry errors, sensor glitches, or fat-fingered inputs. The reason to use MM at 50% rather than M at, say, 20% is the distribution in leverage of those errors:

Y-only contamination (a sensor returns

999for a missing read, or a typo): Huber-M survives up to maybe 25%.Contamination that also moves

x(the same sensor returns(999, 999)): Huber-M’s breakdown drops to essentially zero. MM still survives because its S-init protects against leverage.

MM’s 50% breakdown is the worst-case safety net, not a typical operating point.

Next

04_s_estimator: why the S step is what makes MM achieve 50% breakdown — and what goes wrong if you skip it.